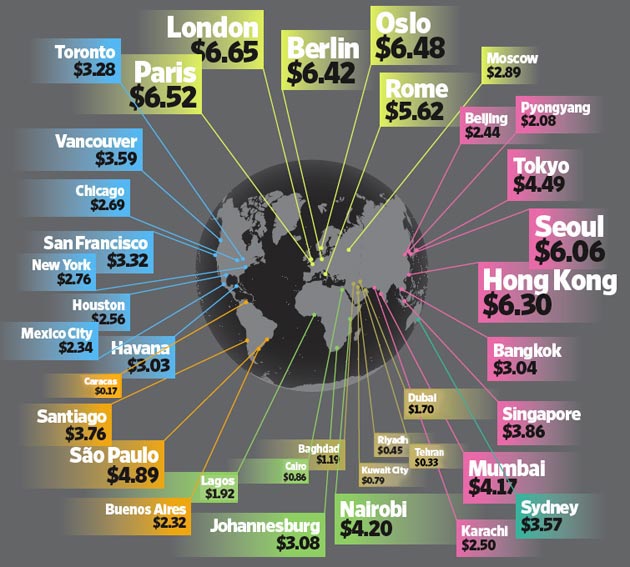

When a major US refinery shuts down, why do oil prices go up? This is counterintuitive. After all, a shut-in refinery means reduced demand for oil, and less demand should mean less price pressure, right? Wrong. Here's an account of the strange ties between oil and gasoline prices. By the way, I could not find the original source of the excellent graphic above, although I know it comes from this blog.

By Peter McKenzie-Brown

The Question of Collusion: Motorists often express concern – call it anger, sometimes – about rising gasoline prices. Citing the reality that neighbouring service stations charge almost identical prices for gasoline, many consumers claim that oil companies illegally collaborate with each other to manipulate gasoline prices. It has frequently been shown, though, that market forces keep local prices the same. If a service station on one street corner charges a penny more per litre than its competitor across the street, motorists will buy from the competitor. It is in each dealer’s self-interest to match the competition’s price.

Economists have no trouble with this explanation of how companies set gasoline prices. It is nonetheless understandable how identical local pump prices cause motorists to suspect collusion by the oil companies – especially when those companies often raise gasoline prices, almost simultaneously, at the beginning of a holiday! Raising prices in anticipation of strong holiday demand is a marketing tactic, however, and not collusion.

Links between Oil and Gasoline Prices: The oil industry’s critics also argue that companies move gasoline prices up quickly when crude oil prices rise, but fail to bring them down when oil prices falter. This argument is also flawed, as a review of the ties between crude oil and gasoline prices in 2006 helps illustrate.

In the week of August 6, the average OPEC crude oil price hit what was then an all-time high: US$71.33 per barrel. That week Canada’s average price of gasoline also reached a peak, at $1.15 per litre. Compared to their averages during the previous two weeks, prices for both commodities rose by about 5 per cent. The following week, OPEC oil and gasoline prices dropped – in both cases, by about 5 per cent. By the week of October 1, which preceded Canada’s Thanksgiving holiday, OPEC oil had dropped by 22 per cent. However, the average price of gasoline for that week had declined to 86 cents – a drop of 27 per cent from its peak price two months earlier. Oil and gasoline prices do track each other, but they are also influenced by other factors. The most important are crude oil prices and taxes.

Refining Problems and Gasoline Prices: In North America there has been a price disconnect between oil and gasoline in recent years. This is partly because the market for gasoline has been strong. This has worsened the limitations in America’s capacity to refine enough gasoline for its consumers.

Canada’s refining centres are at or near Vancouver; Edmonton; Sarnia and Nanticoke, Ontario; Montreal; and St. John, New Brunswick. There are also some smaller refining centres – notably Regina, Saskatchewan and Come-by-Chance, Newfoundland.

Canadians ordinarily produce more than enough gasoline for domestic use. We sometimes import gasoline because refineries need regular maintenance shutdowns or have unexpected operating problems. As the following chart illustrates, our imports are offset by exports to the United States.

The graph also illustrates the seasonal nature of gasoline consumption – we buy far more in the summer than in the winter – and the fact that Canada produces far more gasoline than we consume. Canada exports significant volumes of gasoline, primarily from refineries in Atlantic Canada to the U.S. eastern seaboard. Each year, Canadians consume more than 40 billion litres of gasoline and 25 billion litres of diesel fuel. The bar on the far right of the chart shows Canada becoming a large net-importer of gasoline – for the first time in recent history – in May and June 2006. This occurred because the industry needed to modify many refineries to meet new refining standards. These shutdowns reduced gasoline production just as summer driving was ready to begin, and Canada had to import large volumes to meet demand.

During that summer, motorists witnessed higher, more volatile prices than they had in a long time. Canada was extremely vulnerable to unplanned refinery outages. That brief experience was a small reflection of a large, chronic problem in the United States, and America’s problems affect gasoline prices across the continent.

American Vulnerability: The US has become highly vulnerable to refinery shutdowns, and gasoline prices have developed a volatility that reflects both oil price movements and problems in the refining industry. To some extent, this vulnerability and volatility have splashed across the border into Canada. Gasoline is increasingly a global commodity.

Americans consume about 1.51 billion litres of gasoline every day. The United States is thus the largest gasoline consumer in the world, but it is also the largest refiner. The United States does not produce enough gasoline to meet its own needs, however. It always needs imports, and imported gasoline can be expensive.

“Turnarounds” (scheduled maintenance programs) at US refineries put pressure on international gasoline supply, including supply from Canada. But in recent years unexpected breakdowns at refineries have added urgency to the challenge of meeting consumer needs. These events and stronger demand during the summer driving season contribute to higher prices.

As a rough average, in recent years the US refining sector has operated at 90 per cent of capacity. Put another way, 10 per cent of US refineries have been out of operation at any given time. In that environment, imagine what happens when one or two refineries shut down, reducing capacity use to 89 per cent, say. In a tightly balanced gasoline market, this can cause steep and rapid price increases – something the world witnessed dramatically in 2005, as Hurricane Katrina shut down refineries and closed ports that could have imported gasoline from overseas. The panic that followed briefly took Canadian prices to an all-time high of $1.26 per litre.

A Spiral in Gasoline and Crude Oil Prices: One of the oddest phenomena in the present world of gasoline pricing is its impact on the price of crude oil. As this article has explained, it is logical for gasoline prices to go up along with oil prices. After all, refiners manufacture gasoline from crude oil, and rising input costs contribute to rising total costs.

However, higher gasoline prices also result in higher oil prices. This is less intuitive, for a number of reasons. If a large refinery shuts down, it is reasonable to expect gasoline prices to rise. Less gasoline will be produced, lowering supply; prices will therefore increase. Since there would be less demand for oil to refine, one would normally expect crude oil prices to drop. What actually occurs, however, is the opposite: When a big North American refinery shuts down, both gasoline and oil prices rise. Welcome to the world known to traders as “crack spreads”. “Crack spreads” refers to the spread, or margin, that a refinery can earn by “cracking” (refining) a barrel of oil into such marketable products as gasoline, jet fuel and heating oil. Roughly speaking, three barrels of West Texas oil can be refined into two barrels of gasoline and one barrel of heating oil. If these products rise in value, the value of the barrel of oil they come from will also increase, even if refinery demand for oil has dropped. Thus an off-the-wall oil price spiral: rising crude oil prices increase the price of gasoline, and rising gasoline prices increase the price of oil.

Changing Dynamics: This article has reviewed many factors that are changing the dynamics of gasoline pricing. These factors include rising oil prices. Also, some taxes climb in response to escalating fuel costs, and this further complicates the issue of rising gasoline prices.

We are becoming increasingly reliant on gasoline as our society changes, and there are inefficiencies in the North American petroleum infrastructure that – because petroleum refining and marketing is such a huge industry – will take a long time to strengthen. Of course, this begs the question of whether the oil would be there to supply a larger, more efficient refining sector. That's a question for another day.

{kind=link}